October 18, 2016

Agency

Does The State You Live In Effect Your Insurance Rate?

The world of insurance and how much you pay in insurance premiums can be as confusing as how the dryer can lose so many of your socks. Seriously, is there an internal, hidden abyss in there?

I am not an underwriter for insurance but we can look at different lists of what may affect your auto insurance premium. Over the next couple of weeks, we will compile lists of what does and does not affect auto insurance prices.

Today, let’s look at location.

There are many factors that contribute to your auto insurance premium and what state you live in is a major factor.

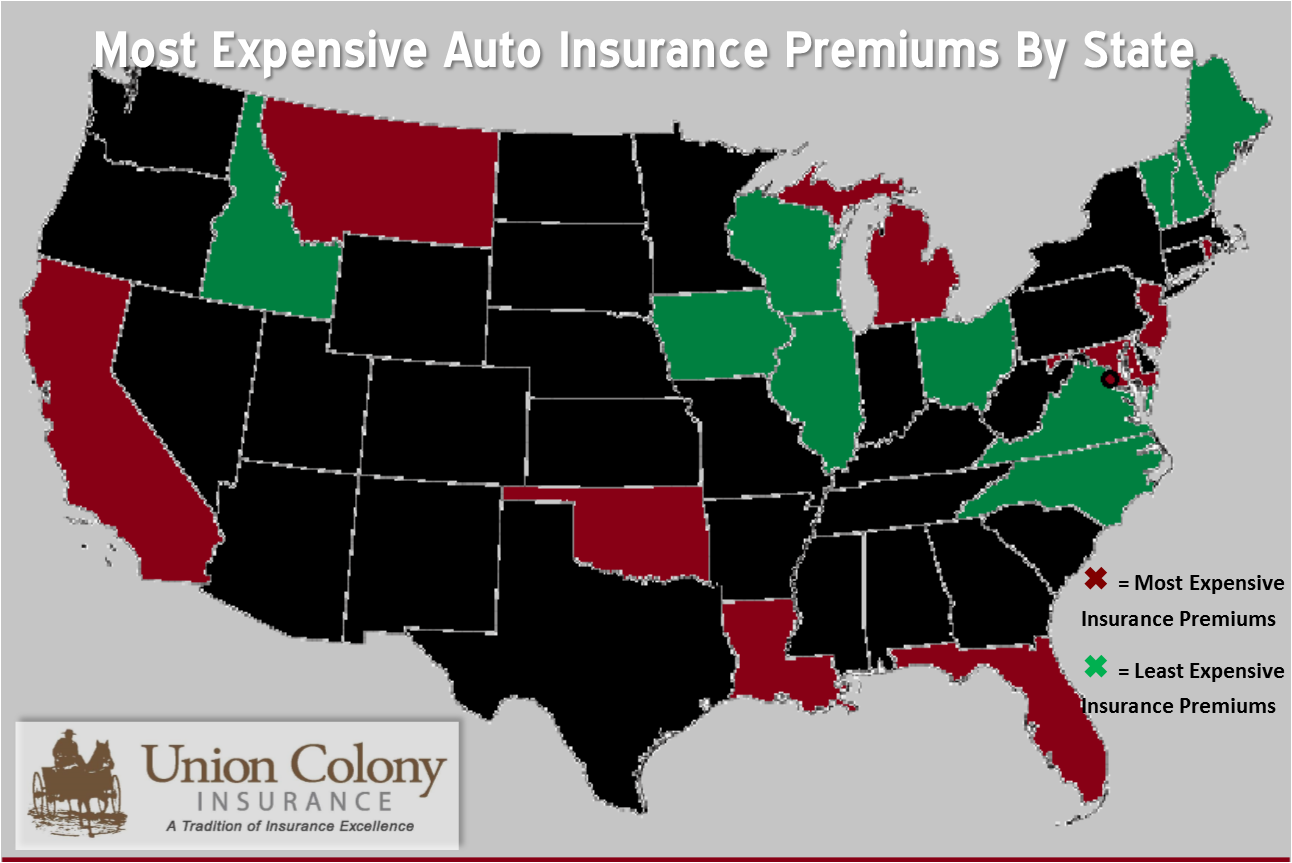

So let’s play the guessing game. Which state do you think has the highest auto insurance premiums and which do you think has the cheapest auto insurance premiums?

Earlier this year, insure.com complied a list of each state by average auto insurance premium. Here is a map of the top 10 most expensive auto insurance premiums by state and the top 10 lowest:

So why does Michigan have the highest insurance premiums and Maine the lowest? Is there a common factor that correlates to insurance premium price?

Well, let’s look at auto accident rates by state. Does the state with the most auto accidents have the highest insurance premiums? A study in 2010 compiled a list of auto accidents by state. We made a map of the U.S. with the top 10 highest accident rate by state and the top 10 lowest accident rate by state:

The only states which cross over having a high insurance premium and a high auto accident rate are Montana, Oklahoma, and Louisiana. Michigan, with the highest insurance premium, only ranked 24th on the list of auto accident rate by state.

Maybe we need to expand our research…

Earlier in the year, a report of the most aggressive drivers by city came out. And in 2014, a study of the rudest drivers by state came out. Let’s look at a map of the most aggressive drivers by city and the rudest drivers by state. The results may surprise you.

Here are a few insights from this latest map:

- Idaho, which is considered one of the rudest states for drivers, has one of the lowest insurance premium.

- Michigan is not considered an aggressive or rude driver state, though has the highest insurance premium.

- Arizona had the most aggressive drivers and is not in the top 10 of highest insurance premiums.

- Montana has relatively calm drivers, but a high accident rate.

So what gives? What factor contributes to why each state has the insurance premium they do? The answer: It depends on a lot of factors.

Let’s look at why the top 3 states have a high insurance premium:

#1) Michigan – Politics

Insurance policies come with unlimited, lifetime medical benefits in Michigan

#2) Montana – Accident Rate

They may not be rude drivers, but they have one of the highest accident rates in the country.

#3) New Jersey – Population Density

New Jersey is number 1 in population density meaning its citizens are more likely to get into an accident. Auto fraud and high medical costs also contribute.

Why do the states with the lowest premiums have the rates they do?

#49) Wisconsin – Lack of Major Cities

A more rural state with a low accident rate in the nation.

#50) Ohio – Home of Insurance Companies

A stable legal and regulatory environment leads to many insurance providers to call Ohio home leading to more competition and lower prices.

#51) Maine – No Serious Weather Conditions

A rural state, with a lack of severe weather conditions to damage a car, keeps prices low.

It’s always interesting to get into the mind of an insurance underwriter. Even though location is a huge factor into why we have the auto insurance premium that we do, there are more factors that contribute to our own personal premium price. We’ll cover more of these reasons in future blog posts.

Any questions about your auto insurance rate, contact us!

Categories: Blog